Index

Why Should Investors Own Healthcare Stocks?

Powerful Long-Term Trends Are Driving Growth In The Sector

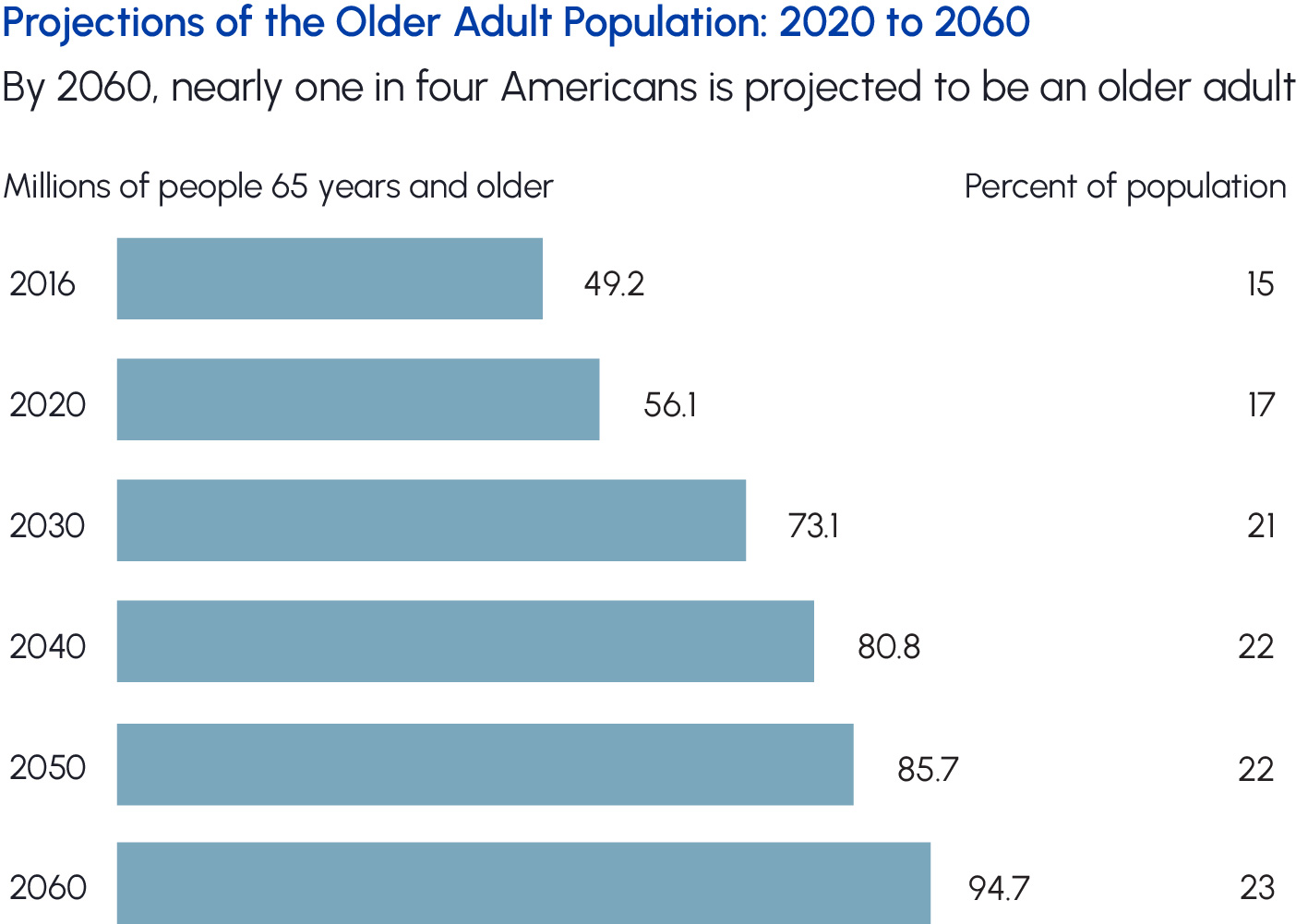

Aging Population

The number of Americans age 65 and older is expected to grow by 30% between 2020 and 2030. By

2034, older adults will outnumber children for the first time in US history. This older cohort spends nearly $20K per year on healthcare products and services – double that of those aged 45 to 64 and quadruple those aged 19 to 44.

|

|

Technological Innovation

The pace of innovation in healthcare has never been faster. Groundbreaking technologies are evolving

rapidly in fields such as genomics, mRNA vaccines, robotic surgeries as well as molecular diagnostics and neuroscience. The scientific community’s unprecedented understanding of human biology, combined with larger data sets and faster information processing capabilities, is expected to yield therapies and procedures that will change medicine.

Healthcare Is Essential

Healthcare spending represents ~20% of US GDP. Immense financial and human resources are required

to ensure equitable access to drugs, doctors and medical equipment for all. The COVID-19 pandemic

highlighted the importance of a well-functioning healthcare system and strengthened R&D commitments from governments, corporations and academic institutions.

Healthier Lifestyle Trends

People view health & wellness through an increasingly broad and sophisticated lens. Overall health encompasses physical and mental health, fitness, nutrition and appearance. Preventative strategies are growing in practice and substantially reduce the risk of chronic diseases such as diabetes, hypertension and heart disease.

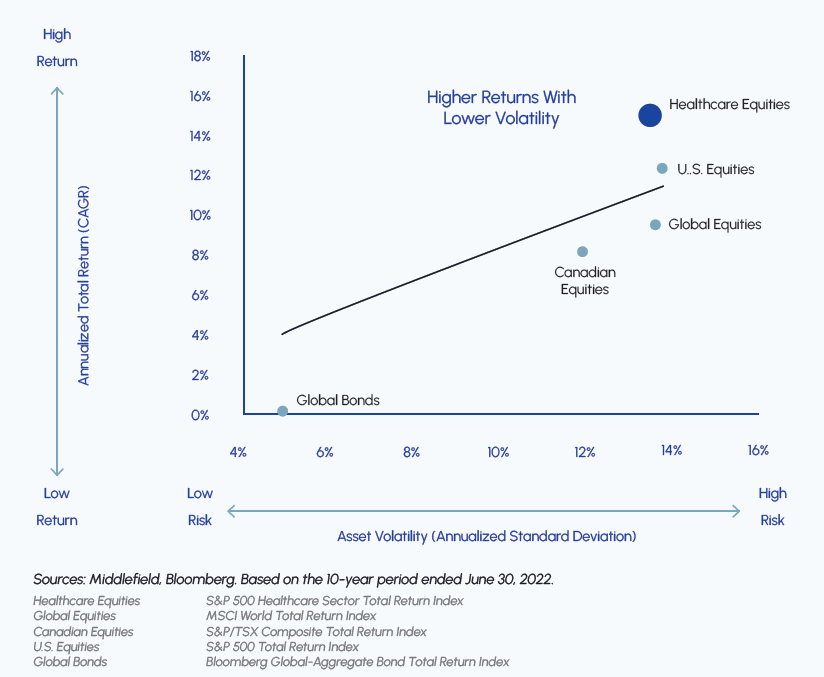

Strong Performance in Good Times and Bad

Healthcare equities offer investors an attractive mix of defensive qualities and growth. Historically, the sector has generated higher total returns while exhibiting lower volatility. Large and established companies in this sector often demonstrate remarkable resilience during market downtrends. For example, during the great financial crisis in 2008-09, sales volumes of pharmaceutical products only declined by 1-3% on average. This inelastic demand is due to the needs-based nature of healthcare products and supports recession-resistant businesses. Healthcare companies also do well during periods of inflation as many of the best firms have low commodity price exposure, high margins and pay growing levels of dividends.

|

Attractive Risk-Adjusted Returns

|

Middlefield’s Healthcare Strategies

Solutions Overview

| Strategy | ETF/Mutual Fund | Ticker/Fund Code | Strategy | ETF/Mutual Fund | Ticker/Fund Code |

|---|---|---|---|---|---|

| Middlefield Healthcare Dividend ETF | ETF | MHCD | Diversified Global Healthcare |

Medium | July 21, 2017 |

| Middlefield Healthcare Dividend Fund | Mutual Fund | MID326 | Diversified Global Healthcare |

Medium | October 23, 2014 |

| Middlefield Health & Wellness ETF | ETF | HWF | Diversified Global Healthcare + Wellness Companies |

Medium | October 20, 2016 |

High Levels of Income

All Middlefield healthcare funds provide investors with attractive levels of monthly income.

Holdings

Middlefield’s healthcare strategies are actively managed portfolios holding approximately 30-45 names with emphasis on stable, mature, large-cap companies that pay and grow their dividends over time.

Exclusive Industry Healthcare Advisor

SSR Health Provides Our Funds With Expert-Driven Healthcare Insights

SSR Relationship

SSR Health is an independent research firm that provides expert analysis of the industry and political landscape impacting the healthcare sector as well as unique comprehension and actionable investment ideas. SSR is highly regarded across the healthcare industry and its client base includes asset managers and government agencies. SSR is an independent research firm and is does not engage in investment banking or sales and trading activities.

SSR Healthcare Lead

Dr. Evans has 20+ years of healthcare industry experience. A former senior pharmaceuticals executive with Roche and top-ranked pharmaceuticals analyst with Sanford C. Bernstein, he was ranked #1 by both Bloomberg and Institutional Investor for his thought-leading industry coverage.

|

|

Healthcare Areas We Like

Powerful Secular Trends Are Driving Opportunities In The Following Sub-Sectors

Pharmaceutical companies generate stable and predictable earnings, carry low financial leverage and consistently grow their dividends.

Biotech

The biotechnology industry is on the cusp of a multi-decade innovation cycle which is expected to yield groundbreaking therapeutics and treatments.

Pharmaceuticals

Pharmaceutical companies generate stable and predictable earnings, carry low financial leverage and consistently grow their dividends.

Equipment & Supplies

Robust innovation, expanding end markets and pandemicrelated backlogs result in higher average growth rates.

Life Science Tools & Service

Elevated R&D spending from industry, government and academic centres support robust genomics, DNA sequencing and molecular diagnostics innovation.

Managed Care

Subsiding COVID-19 hospitalizations and low unemployment improves the case mix and should lead to higher utilization of healthcare services.

Disclaimer

This material has been prepared for informational purposes only without regard to any particular user’s investment objectives or financial situation. This communication constitutes neither a recommendation to enter into a particular transaction nor a representation that any product described herein is suitable or appropriate for you. Investment decisions should be made with guidance from a qualified professional. The opinions contained in this report are solely those of Middlefield Limited (“ML”) and are subject to change without notice. ML makes every effort to ensure that the information has been derived from sources believed to reliable, but we cannot represent that they are complete or accurate. However, ML assumes no responsibility for any losses or damages, whether direct or indirect which arise from the use of this information. ML is under no obligation to update the information contained herein. This document is not to be construed as a solicitation, recommendation or offer to buy or sell any security, financial product or instrument.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund and ETF investments. Please read the prospectus and publicly filed documents before investing. Mutual funds and ETFs are not guaranteed, their values

change frequently, and past performance may not be repeated. You will usually pay brokerage fees to your dealer if you purchase or sell shares of an investment fund on the Toronto Stock Exchange or alternative Canadian trading platform (an “exchange”). If the shares are purchased or sold on an exchange, investors may pay more than the current net asset value when buying shares of the investment fund and may receive less than the current net asset value when selling them. There are ongoing fees and expenses associated with owning shares of an investment fund. An investment fund must prepare disclosure documents that contain key information about the fund. You can find more detailed information about the fund in the public filings available at www.sedar.com. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Certain statements in this press release may be viewed as forward-looking statements. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, intentions, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as “expects”, “is expected”, “anticipates”, “plans”, “estimates” or “intends” (or negative or grammatical variations thereof), or stating that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved) are not statements of historical fact and may be forward-looking statements. Forward-looking statements are subject to a variety of risks and uncertainties which could cause actual events or results to differ from those reflected in the forward-looking statements including as a result of changes in the general economic and political environment, changes in applicable legislation, and the performance of each fund. There are no assurances the funds can fulfill such forward-looking statements and the funds do not undertake any obligation to update such statements. Such forward-looking statements are only predictions; actual events or results may differ materially as a result of risks facing one or more of the funds, many of which are beyond the control of the funds.